Sovereign Tax Architecture: The 2026 Comprehensive Guide to WHT, VAT, and CIT in Saudi Arabia

The tax ecosystem in the Kingdom of Saudi Arabia in 2026 serves as the fundamental pillar for financing mega-projects and achieving fiscal sustainability within the framework of Vision 2030. Understanding the core differences between Withholding Tax in Saudi Arabia (WHT), Value Added Tax in Saudi Arabia (VAT), and Corporate Income Tax in Saudi Arabia (CIT) is not merely an accounting necessity; it is a strategic decision that directly impacts Business liquidity Saudi Arabia. In 2026, the Zakat, Tax and Customs Authority (ZATCA) transitioned to a phase of "Full Tax Intelligence," where real-time linking is established between all financial transactions and government systems. This evolution imposes a mandatory requirement on investors for proactive compliance to avoid financial penalties and ensure business continuity.

At Motaded Limited (Motaded), in our capacity as a leading Legal consultant in Saudi Arabia and a certified business incubator, we provide this encyclopedic reference to ensure that your companies are established and managed according to the highest standards of tax and sovereign integrity. We rely on the updated regulations and laws of 2026 to offer a clear roadmap for international capital. The Kingdom's tax landscape is designed to be transparent, predictable, and fair, aligning with the best practices of the G20 nations, thereby fostering a secure environment for a successful Saudi company formation.

1. The General Tax Landscape in Saudi Arabia 2026

The year 2026 witnessed a radical shift in how companies interact with taxes in the Kingdom, where "Digital Compliance" became the only accepted standard. The Saudi tax system aims to create a transparent investment environment that rivals the best international practices. The diversity between direct taxes like Corporate Income Tax in Saudi Arabia and indirect taxes like VAT, in addition to Withholding Tax in Saudi Arabia on international transactions, creates a regulatory network that ensures tax justice. Today, foreign investors find a clear system that separates "Zakat," paid by Saudi/GCC partners, and "Taxes," which the foreign share is subject to. This clarity facilitates long-term financial planning and risk assessment.

This legislative maturity has significantly contributed to increasing the attractiveness of Business setup in Saudi Arabia for global groups seeking financial and legal stability. The digital infrastructure provided by ZATCA allows for seamless filing and automated verification, reducing the administrative burden on businesses. Furthermore, the integration of tax data with other government platforms, such as the Ministry of Commerce and the Ministry of Investment, ensures that a company’s tax status is a true reflection of its operational health. For a foreign firm, this means that transparency is rewarded with faster access to government services and greater credibility in the local market, making Market entry into the Saudi Arabia a highly structured and secure process.

2. Corporate Income Tax in Saudi Arabia Tax (CIT): Concepts and Sovereign Rates

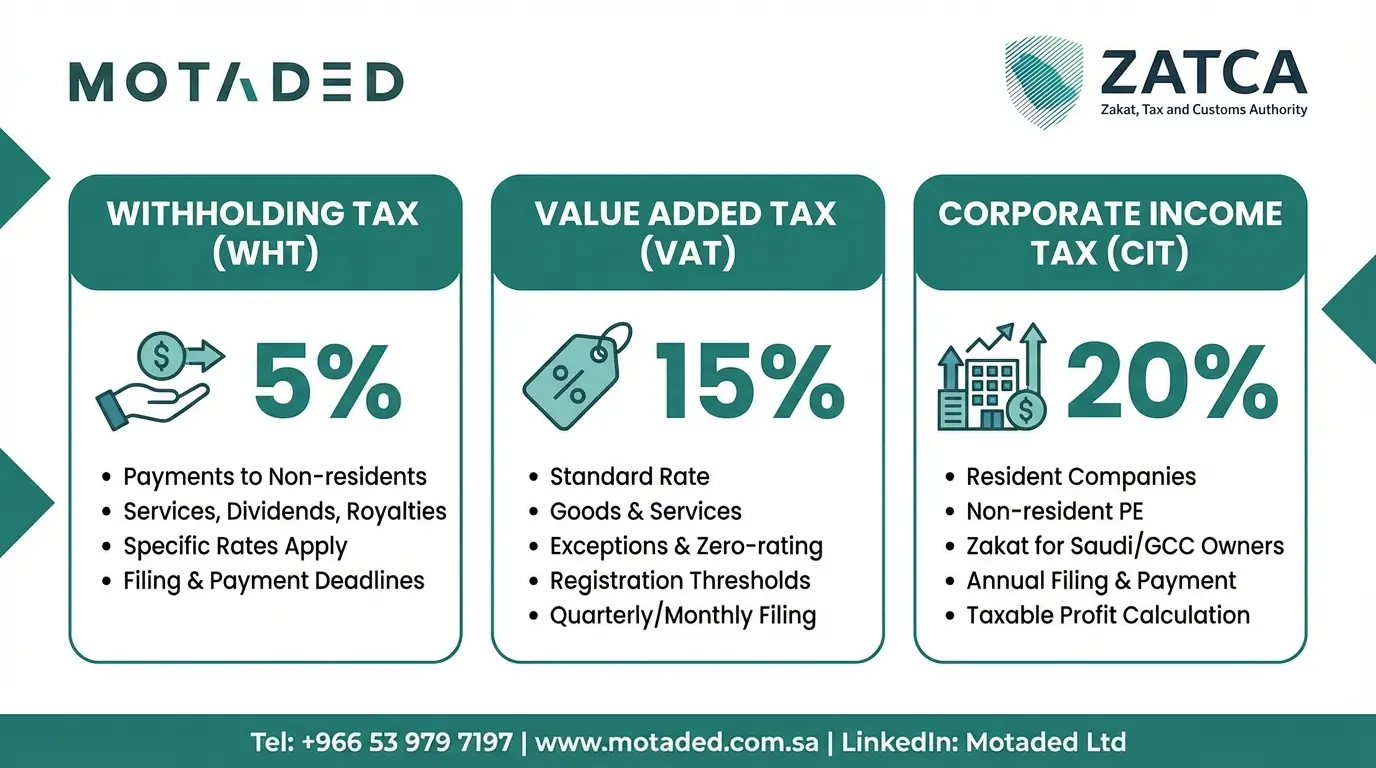

Corporate Income Tax in Saudi Arabia (CIT) is the primary tax imposed on the net profits of foreign companies operating in the Kingdom or the foreign partner's share in mixed companies. In 2026, the sovereign rate for income tax remains fixed at 20% of the tax base (adjusted net profit). This tax is not levied on total revenue but on profits after deducting legally permissible expenses. The accuracy of preparing financial statements and verifying deductible expenses is the key to maintaining Business liquidity Saudi Arabia. Tax returns must be submitted annually via the ZATCA portal and must be supported by a report from a licensed certified public accountant to ensure data accuracy and integrity before the authority.

The 20% rate is highly competitive on a global scale, especially when considering the lack of personal income tax for individuals in the Kingdom. For the investor, this means that the return on investment (ROI) remains attractive while contributing to the national infrastructure. ZATCA has also introduced various "Advance Tax Rulings" that allow companies to clarify the tax treatment of complex transactions before they occur, providing an extra layer of certainty. This proactive approach to ZATCA Compliance is vital for large-scale infrastructure projects and long-term industrial investments. By aligning corporate accounting with Saudi tax laws from the outset, companies can optimize their tax positions and ensure that their Saudi company formation is financially robust and legally sound.

3. Value Added Tax (VAT): Implementation and the 15% Rate

Value Added Tax in Saudi Arabia (VAT) is an indirect tax imposed on all goods and services purchased and sold by entities, with limited exceptions. The standard rate in Saudi Arabia is 15%. In 2026, the management of this tax relies entirely on the "Fatoora" e-invoicing system, where collected and paid taxes are recorded in real-time. Companies whose annual supplies exceed the mandatory registration threshold (SAR 375,000) must register for VAT and submit periodic returns (monthly or quarterly). Managing "Input and Output" taxes accurately ensures the company can recover excess amounts and protect its cash flows from freezes resulting from payment delays or filing errors.

The VAT system is designed to be self-regulating, but it requires high levels of technical integration. In 2026, the "Phase 2" of e-invoicing is fully operational, meaning every invoice is cryptographically signed and transmitted to ZATCA's servers instantly. This transparency prevents the accumulation of tax debt and ensures that the 15% rate is applied consistently across the supply chain. For businesses engaged in Business setup in Saudi Arabia, especially in the retail or service sectors, VAT compliance is a daily operational priority. Our team at Motaded provides the technical and legal oversight necessary to ensure that your billing systems are perfectly synchronized with the national grid, safeguarding your Business liquidity Saudi Arabia and ensuring a clean audit trail for any future sovereign inspections.

4. Withholding Tax in Saudi Arabia (WHT): Engineering International Transactions

Withholding Tax in Saudi Arabia (WHT) is one of the most precise and sensitive taxes in the Business setup in Saudi Arabia framework. This tax is imposed on amounts paid from a resident entity in Saudi Arabia to a non-resident entity in exchange for services provided from abroad. Rates vary based on the service type; for instance, the rate for Royalties is 15%, while Management fees are taxed at 20%, and Technical and Consulting services at 5%. The responsibility for withholding and remitting the tax to the authority lies with the resident company in Saudi Arabia within the first 10 days of the month following payment. Failure to understand this tax can lead to unexpected costs for the foreign investor.

WHT often becomes a point of negotiation in international contracts. As a Legal consultant in Saudi Arabia, we ensure that our clients’ contracts clearly define which party bears the tax burden—whether the payment is "net of tax" or "inclusive of tax." This clarity is essential for preserving the financial viability of cross-border service agreements. In 2026, ZATCA's automated systems can detect payments to foreign entities by auditing bank records and commercial contracts, making non-disclosure a high-risk strategy. By correctly classifying services—distinguishing between technical work (5%) and management (20%)—companies can avoid overpaying and ensure their Market entry into the Saudi Arabia is optimized for fiscal efficiency and total compliance with sovereign regulations.

5. The Language of Numbers: Compliance and Collection Statistics 2026

Official data issued by ZATCA for 2025 and the first quarter of 2026 reflects the high efficiency of the tax system:

| Tax Type | Digital Compliance Rate | Impact on Public Budget |

|---|---|---|

| Value Added Tax (VAT) | 99% (Via E-Invoicing) | Largest non-oil revenue source |

| Corporate Income Tax (CIT) | 95% (Audited Returns) | Steady growth with foreign FDI |

| Withholding Tax (WHT) | 92% (Documented Intl. Transactions) | High regulation of external service flows |

These figures confirm that ZATCA Compliance has become a corporate culture in Saudi Arabia, reducing the risks of the "shadow economy" and enhancing market transparency. This reflects positively on the Kingdom's evaluation in global financial indices and makes it easier for companies to obtain bank financing at competitive rates. For investors, these statistics provide proof of a stable and well-regulated market. A high compliance rate in the Kingdom ensures a level playing field where all competitors follow the same rules, which is a major factor in the success of Saudi company formation. At Motaded, we use these data points to help our clients benchmark their own compliance performance against the national average, ensuring they remain in the "safe zone" of sovereign audits.

6. The Role of Motaded Limited in Tax Compliance

As a Legal consultant in Saudi Arabia and a certified business incubator, we at Motaded Limited (Motaded) play a vital role in protecting our clients from tax risks. We do not just provide advice; we perform "Compliance Engineering" by:

Reviewing international contracts to ensure the party responsible for Withholding Tax in Saudi Arabia (WHT) is clearly defined.

Overseeing the linking of accounting systems with the "Fatoora" platform to ensure the accuracy of Value Added Tax in Saudi Arabia (VAT) returns.

Providing consultations on profit and expense structuring to ensure the submission of an accurate and fair Corporate Income Tax in Saudi Arabia (CIT) return.

This role ensures that the investor's Saudi company incorporation is built on absolute financial transparency, protecting them from penalties that can reach high percentages of the non-disclosed amounts. Our incubator status also allows us to guide startups through the initial "tax-free" or "tax-incentivized" periods offered in certain economic zones. By integrating tax planning into the early stages of Business setup in Saudi Arabia, we help our clients build a scalable and sustainable business model that is ready for the rigors of 2026's digital tax environment. We act as your primary shield against procedural errors, ensuring your focus remains on growth while we handle the complexities of sovereign tax compliance.

7. E-Invoicing (Fatoora): Integration and Linking Phase 2026

In 2026, all establishments subject to VAT entered the "Integration and Linking Phase." This phase means that every invoice issued by a company must be sent immediately to ZATCA's systems for approval and encryption before being delivered to the customer. This digital system has completely eliminated paper and manual invoices, ensuring real-time monitoring of sales volume and collected taxes for the authority. For the investor, this system provides protection against accounting manipulation and facilitates the preparation of tax returns, as the data is pre-registered with the authority. Technical commitment to e-invoicing is an integral part of a successful Business setup in Saudi Arabia.

This real-time reporting mechanism has significantly reduced the time required for VAT audits. Because ZATCA already has a record of every transaction, the "year-end" audit becomes a matter of verification rather than investigation. However, this also means that errors in the billing software can lead to immediate compliance flags. We at Motaded work with technical partners to ensure that our clients' ERP systems are fully certified and compatible with the latest ZATCA API standards. This technical readiness is a critical component of Saudi company formation in the digital era. By ensuring that your e-invoicing is perfect from the first transaction, you establish a reputation for integrity and professionalism with the sovereign financial regulators.

8. International Agreements and Preventing Double Taxation

The Kingdom of Saudi Arabia has signed more than 50 international agreements for the prevention of double taxation with various countries worldwide. These agreements gain maximum importance when discussing Withholding Tax in Saudi Arabia (WHT) and Corporate Income Tax in Saudi Arabia (CIT). These treaties allow foreign investors to reduce withholding rates or even obtain exemptions in certain cases, and ensure they do not pay tax twice on the same income in Saudi Arabia and their home country. We at Motaded assist investors in obtaining "Tax Residency Certificates" and applying international treaty provisions, maximizing their transferable profits and achieving the highest levels of financial efficiency for their investments.

Applying for treaty benefits requires a thorough understanding of both the Saudi tax law and the specific terms of the bilateral agreement. Often, an investor must prove that the non-resident entity is the "beneficial owner" of the income to qualify for a lower WHT rate. Our legal team handles these complex filings, ensuring that our clients are not over-taxed on their global operations. For a company undergoing Saudi company incorporation, utilizing these treaties can significantly increase the "Net After Tax" profit, making the Saudi market more competitive compared to other jurisdictions. This level of fiscal optimization is a core part of our consultancy, ensuring that your Market entry into the Saudi Arabia is as profitable as it is compliant.

9. Withholding Tax in Saudi Arabia on Technical and Management Services

Many investors fall into confusion between the types of services subject to Withholding Tax (WHT). In 2026, definitions have been further refined; "Technical and Technological Services" are subject to a 5% tax, while "Management Fees" are subject to a 20% rate. This vast difference requires the precise drafting of international service agreements. If a management service is mistakenly classified as technical, the authority may impose tax differences and heavy delay penalties. Our role as a Legal consultant in Saudi Arabia is to review these contracts before signing to ensure the correct classification and protect the company's cash flows from sudden tax claims.

ZATCA's criteria for "Management Fees" are broad, often including any service that involves the oversight or direction of the Saudi entity's operations. Conversely, technical services usually involve a specific transfer of knowledge or a specialized technological task. Distinguishing between these two in a contract is an art form that requires deep legal and accounting expertise. We help our clients document the "substance" of the service to support the chosen tax rate during a sovereign audit. This proactive documentation is vital for preserving Business liquidity Saudi Arabia, as it prevents the freezing of funds during lengthy disputes. By getting the WHT classification right from the start, you ensure a smoother financial relationship with both your foreign suppliers and the Saudi tax authorities.

10. Zakat Base vs. Tax Base

A fundamental concept in Saudi company formation is the distinction between the Zakat base and the Tax base. The share of a Saudi or GCC partner is subject to "Zakat" at a rate of 2.5% of the Zakat base (which includes capital, profits, and reserves minus fixed assets), while the share of a foreign partner is subject to Corporate Income Tax in Saudi Arabia (CIT) at 20% of the net profit. In mixed companies, profits and the financial base are divided according to the ownership percentage. This division requires a sophisticated accounting system that can accurately separate Zakat obligations from tax obligations, which we provide at Motaded through our integrated accounting and tax services to ensure fairness and integrity in the distribution of financial burdens among partners.

Managing a mixed-ownership company in 2026 requires two parallel sets of calculations for every fiscal year. The "Adjusted Net Profit" for tax purposes may differ from the "Zakat Base" due to different rules regarding the treatment of long-term investments and liabilities. Our specialized accountants ensure that each partner's liability is calculated to the cent, preventing internal shareholder disputes and ensuring that the entity as a whole remains in ZATCA Compliance. This level of detail is particularly important for large joint ventures where millions of Riyals are at stake. By providing clear and transparent reporting, we help our clients maintain healthy shareholder relations and a spotless record with the sovereign regulators.

11. Tax Appeals and Judicial Committees

The Saudi system provides a fair mechanism for appealing ZATCA decisions. If there are tax differences resulting from the authority's audit of Value Added Tax in Saudi Arabia (VAT) or Corporate Income Tax in Saudi Arabia (CIT), the entity has the right to appeal within 60 days before the authority. If rejected, the case can be escalated to the "General Secretariat of Tax Committees." In 2026, these sessions are held entirely digitally and are characterized by rapid dispute resolution. We at Motaded Limited represent our clients in tax dispute cases, preparing legal and accounting memos supported by evidence and regulations to ensure rights are recovered and the company is protected from inaccurate tax decisions, enhancing confidence in the Kingdom's judicial tax environment.

The appeal process is highly technical and requires a combination of legal arguments and forensic accounting. Often, a dispute arises from a difference in the interpretation of a specific clause in the tax law or a double taxation treaty. Our legal team includes former tax officials and expert litigators who understand the "mindset" of the committees. We ensure that our clients' cases are presented with the highest degree of professionalism. This judicial recourse is a cornerstone of the Business setup in Saudi Arabia, as it ensures that even in a digital and automated environment, the rule of law and the right to a fair hearing remain paramount. This protection is a major reassurance for foreign capital entering the Kingdom.

12. Impact of Taxes on "Nitaqat" and Government Tenders

Tax compliance (ZATCA Compliance) has become a basic condition for entering major government tenders and obtaining compliance certificates from the Ministry of Human Resources. A company that has a default in paying VAT or Withholding Tax is deprived of obtaining a clean "Saudization Certificate" and may be excluded from sovereign contracts. Tax commitment indirectly enhances a company's classification in the "Nitaqat" system by proving financial solvency and administrative regularity. We ensure at Motaded that our clients' tax files are entirely "clean," opening doors for them to contract with government agencies and mega-corporations like Aramco and NEOM, enhancing the company's prestige as a compliant and honest entity.

In 2026, a "Tax Clearance Certificate" is a mandatory document for the final release of payments on government projects. If your company is not in good standing with ZATCA, your Business liquidity Saudi Arabia could be severely impacted as payments are withheld by the client. We provide a "Continuous Compliance" service where we monitor your tax status monthly, ensuring that any issues are resolved before they become hurdles to business growth. For companies involved in Saudi company formation, being "Tender-Ready" from day one is a competitive necessity. By maintaining a perfect tax record, you not only avoid penalties but also position your firm as a reliable and preferred partner for the Kingdom's most ambitious projects.

13. Frequently Asked Questions (FAQ) about Taxes

1. Are the salaries of foreign employees subject to Corporate Income Tax in Saudi Arabia (CIT)?

No, Income Tax is imposed on company profits, not individual salaries. Employees are subject to the Social Insurance system (GOSI), and there is no personal income tax on salaries in Saudi Arabia in 2026.

2. When should Withholding Tax (WHT) be remitted to the authority?

The tax must be withheld and remitted within the first ten days of the month following the month in which the payment was made to the non-resident supplier.

3. Is VAT paid on purchases refundable?

Yes, registered entities can deduct the VAT paid on their inputs (purchases) from the VAT collected on their sales and request a refund of the surplus from the authority.

4. How does the 20% Income Tax rate affect investment attractiveness?

The 20% rate is considered very competitive globally, especially with the existence of exemptions and incentives in industrial and technical sectors, making Market entry into the Saudi Arabia a very profitable option.

14. Data Integrity and Strategic Conclusion

Managing files for Withholding Tax, Value Added Tax, and Corporate Income Tax in Saudi Arabia in 2026 requires a partner who possesses legal precision and technical expertise. The Kingdom of Saudi Arabia has presented a tax system that combines firmness and fairness, and success in it depends on "absolute transparency." Commitment to official data and avoiding wrong guesswork is the only guarantee for growing your investments away from legal risks.

Motaded Limited (Motaded) remains your compass toward full compliance as a Legal consultant in Saudi Arabia and a certified business incubator. We guarantee you the building of a tax-compliant and sovereign commercial entity to be an active part of the future of the Saudi economy.